Alex Quick Thoughts - Q1 2025 earnings on target. Netflix is claimed by a fund manager to be the best potential tech stock for 2025 with the ongoing trade war. Oh, by the way - I made that claim here on the club before those highly paid specialists, lol. Wish I knew this sooner (or could see the future) and I would have swapped half my Nvidia to hedge with Netflix.

📰 Market Context

Netflix stock has demonstrated remarkable resilience in a volatile market, currently trading at $918.29 after surging approximately 4% following its strong Q1 2025 earnings report. The company's strategic shift from subscriber-growth metrics to profitability and engagement metrics has been well-received by investors, positioning it as both a defensive and growth tech stock during broader market uncertainty. Netflix's stock is up 9% year-to-date, outperforming many tech peers in the current macroeconomic environment.

Key Catalysts:

Strong Q1 2025 earnings beat with 12-13% YoY revenue growth and 25% EPS growth

Strategic pivot to emphasizing profitability metrics over subscriber numbers

Reed Hastings' transition from executive chairman to non-executive chair, signaling confidence in current leadership

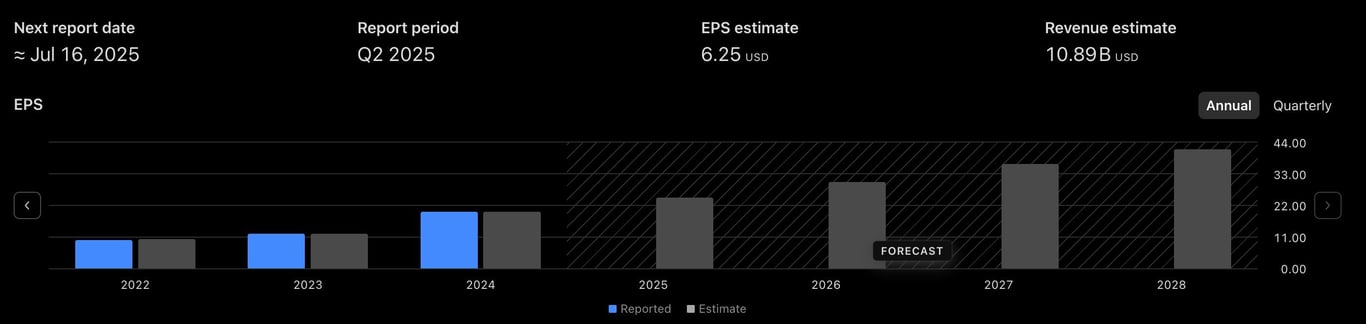

📊 Latest Earnings Update

Netflix delivered a robust Q1 2025 earnings report that exceeded Wall Street expectations across all key financial metrics. Revenue reached $10.54 billion, slightly above analyst estimates, while EPS surged to $6.61, significantly outpacing the $5.68-$5.71 consensus. The company's operating margin expanded to an impressive 31.7%, up from 28.1% in the previous year, demonstrating Netflix's ability to drive operational efficiency while maintaining growth. Management's guidance for Q2 and full-year 2025 remains upbeat, underscoring confidence in continued momentum.

Earnings Highlights:

Revenue: $10.54 billion (+12-13% YoY) vs $10.50 billion expected

EPS: $6.61 (+25% YoY) vs $5.68-$5.71 expected

Operating Income: $3.3 billion (+27% YoY) vs $3.0 billion expected

The BuyTrigger metrics for Netflix reveal a company that has reached a critical inflection point, with its current market price now exceeding both the BuyTrigger and Value Trigger prices. This suggests Netflix has transitioned from a value opportunity to fairly valued based on current fundamentals. With strong performance and recommendation scores above 70, the company demonstrates operational excellence despite moderate risk levels. The recent price appreciation reflects the market's recognition of Netflix's improved profitability metrics and confidence in its long-term growth trajectory.

BuyTrigger Metrics:

Current Price: $918.29 vs BuyTrigger: $900.00 (2.03% above)

Value Trigger: $902.01 (1.80% below current price)

Risk Score: 51/100 - Moderate risk profile balanced by strong market position

Recommendation: 86/100 - Strong buy recommendation despite current valuation

Ready for More Professional Investment Analysis Like This?

Join the BuyTrigger Club 2.0 today and gain access to our complete library of in-depth stock analyses!

For just $150 per year (that's only $12.50 per month), you'll receive professional-grade investment research that typically costs thousands elsewhere. Our proprietary BuyTrigger framework identifies optimal entry points and value targets for high-potential stocks across various sectors, helping you make smarter investment decisions with confidence.

Members receive:

Weekly new stock analyses with complete BuyTrigger metrics

Telegram dynamic BuyTrigger and ValueTrigger updates

BuyTrigger 2.0 Database full access

Priority access to our value-based investment methodology

Exclusive market context updates and catalyst tracking

Why pay premium broker fees for biased research when you can access independent, data-driven analysis for less than the cost of a streaming service? Our members consistently report making back their membership fee many times over through just a single well-timed investment.

Netflix continues to benefit from several fundamental growth drivers that support its premium valuation. The company's unmatched scale in global streaming allows it to amortize content costs across its massive user base, creating significant operating leverage. Strategic price increases across various tiers, including the first price rise for the ad-supported tier, demonstrate Netflix's pricing power. The company's sophisticated content recommendation algorithm and diverse programming slate continue to drive engagement, reducing churn and supporting sustained revenue growth.

Growth Drivers:

Global scale creating operating leverage with 31.7% operating margins

Successful implementation of pricing strategy across subscription tiers

Content diversification strategy balancing high-cost originals with efficient programming

Streaming adoption accelerating in international markets, particularly APAC (+23% YoY)

Shift from subscriber growth to profitability metrics across the streaming industry

Increased focus on advertising revenue streams complementing subscription models

🏆 Competitive Positioning

Netflix maintains its leadership position in the streaming landscape through continued innovation and efficient content monetization. With over 302 million global subscribers as of late 2024, the company possesses unrivaled scale advantages. Its strategic shift to emphasize financial metrics over subscriber growth aligns with its maturity phase, focusing on profitability and capital efficiency. However, intensifying competition and the high cost of content creation represent persistent challenges that require vigilant management.

Bull Case:

Unmatched global scale with 302 million subscribers enabling superior content amortization

Successful transition to a balanced growth and profitability model with 31.7% operating margins

Strong free cash flow generation of $2.66 billion in Q1 alone, supporting content investment

Bear Case:

Increasing competition from both established players and new entrants in the streaming space

Potential market saturation in mature regions like North America

💡 Investment Thesis

Netflix represents a compelling investment case based on its successful evolution from a pure growth story to a balanced growth and profitability narrative. The company has effectively navigated the challenging transition from subscriber acquisition to monetization and profit maximization. With current prices slightly above the BuyTrigger level, the investment thesis now rests on Netflix's ability to continue driving operational efficiency while maintaining double-digit revenue growth. Management's ambitious target to double revenue to $80 billion by 2030 and reach a $1 trillion market cap appears increasingly achievable given the company's execution excellence and expanding margins. The key investment question has shifted from "Can Netflix grow subscribers?" to "Can Netflix continue to extract more value from its existing subscriber base while expanding margins?"

🎯 Action Plan

Based on the BuyTrigger framework, Netflix requires a nuanced investment approach given its current valuation slightly above both BuyTrigger and Value Trigger levels. The stock presents a hold opportunity for existing investors and a measured entry point for new investors seeking exposure to a high-quality streaming leader. With the stock trading at $918.29 versus a BuyTrigger of $900.00, investors should consider establishing partial positions at current levels while keeping dry powder for potential market volatility.

Investment Approach:

Buy Strategy: Consider initiating or adding to positions at current levels with a preference for increasing allocation on any pullbacks toward the $900.00 BuyTrigger price

Value Recognition: While the Value Trigger price of $902.01 has been exceeded, long-term fundamental value remains compelling given operating margin expansion

Portfolio Integration:

Portfolio Category: "Disruptive Technology" with "Mature Growth" characteristics, suitable for investors seeking balanced growth and stability

Allocation Guidance: 3-5% position sizing appropriate for core holdings in growth-oriented portfolios

Risk Balancing: Pair with more stable value investments to offset Netflix's moderate risk profile (Risk Score: 51/100)

Long-Term Perspective:

Investment Horizon: 3-5 year outlook aligned with management's 2030 revenue target of $80 billion

Fundamental Reassessment Triggers: Operating margin contraction below 25%, material slowdown in APAC growth, or significant FCF deterioration

🔮 Outlook Summary

Netflix's outlook remains positive as the company continues to execute on its long-term strategy of balancing growth with profitability. The shift away from subscriber reporting indicates management's confidence in its ability to drive financial performance through multiple levers beyond simple subscriber growth. Regional revenue diversification, with particularly strong momentum in APAC (+23% YoY) and EMEA (+15% YoY), provides multiple growth vectors. The company's strategic pivot toward emphasizing engagement and financial metrics aligns perfectly with its maturing business model.

Key Milestones:

Achieving 30%+ operating margins consistently through 2025-2026

Revenue acceleration toward $44.5 billion for full-year 2025

Catalysts to Monitor:

Successful implementation of new advertising tier monetization strategies

Potential headwinds from increased competition or macroeconomic challenges

Netflix represents a premium asset in the digital entertainment landscape that has successfully transitioned from pure growth to balanced growth and profitability. While the stock is currently trading slightly above its BuyTrigger price, the company's execution excellence, expanding margins, and long-term growth trajectory justify its premium valuation. Investors should view Netflix as a core holding in growth-oriented portfolios, representing a company that has mastered both content creation and efficient monetization at global scale. The combination of strong financial metrics, operational efficiency, and clear strategic vision positions Netflix for continued success in the evolving streaming landscape.

This report is provided for informational purposes only and does not constitute investment advice. Investors should conduct their own research and consult with a financial advisor before making investment decisions.

VIX crossed 22 and the death cross is widening. Here are 17 A-rated and B+ stocks currently below their BuyTrigger entry price — beyond the usual MAG7 names everyone already owns.

Which stocks are stretched beyond fair value? Quantitative analysis of 15 positions trading at 80-192% premium including LYFT, SoFi, CrowdStrike, and Lam Research. Risk management insights.

While everyone chases last year's winners like Micron (+213%), these 7 quality stocks are sitting at BuyTrigger levels with fresh 2026 catalysts. NVDA, META, AMZN, UBER, VRT, TSM, EQT.